Table of Contents

Introduction

Insurance basics are something most people overlook — until the moment they desperately need them.

Picture this: You wake up one morning to find your car has been totaled in a parking lot accident. Or worse, you land in the hospital unexpectedly and face a bill that runs into tens of thousands of dollars. Without insurance, moments like these can wipe out years of savings in a single day.

That is why understanding insurance basics is not just useful — it is genuinely important for your financial survival.

In this guide, you will learn exactly what insurance is, how it works, why it matters for your financial future, the most common types available, and the key terms you need to know before buying any policy. Whether you are buying your first policy or simply trying to make sense of what you already have, this article gives you the clear, honest information you need.

Let us start from the beginning.

1. What Is Insurance?

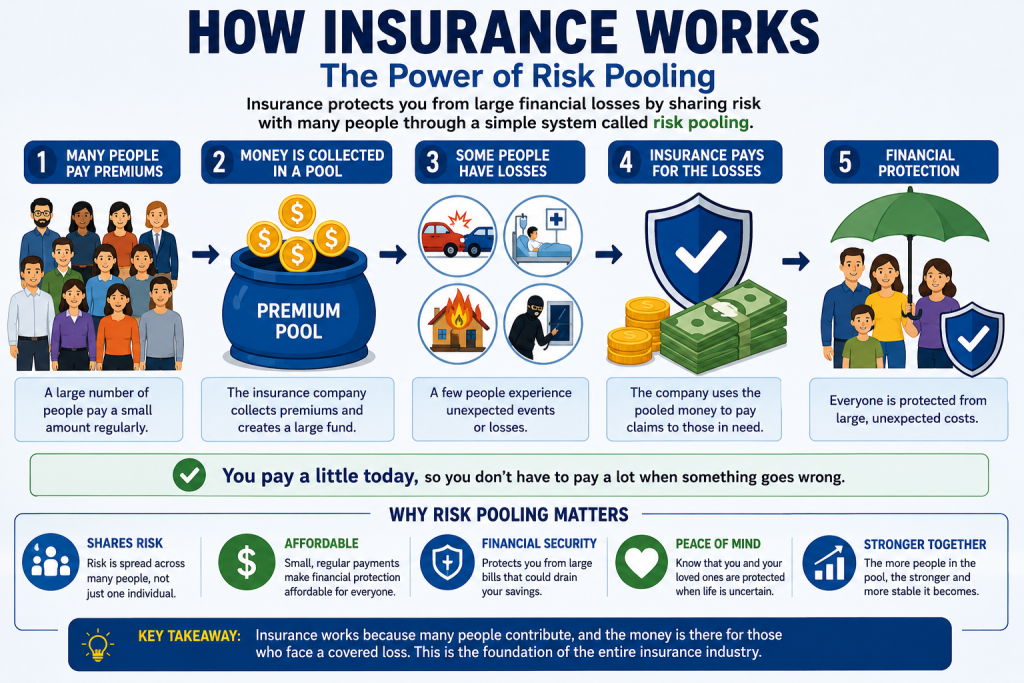

Insurance basics begin with one simple idea: protecting yourself from financial loss by sharing risk with a large group of people.

When you buy an insurance policy, you pay a regular fee — called a premium — to an insurance company. In return, that company agrees to cover certain financial losses if a specific event happens to you, such as an accident, illness, or property damage.

The insurance company collects premiums from a large number of policyholders. Since not everyone experiences a major loss at the same time, the company uses the pooled money to pay out claims to those who do.

This system is called risk pooling, and it is the foundation on which the entire insurance industry is built.

In plain terms: You pay a little every month so that you do not have to pay a lot all at once when something goes wrong.

Insurance is used across nearly every area of personal and business finance — from protecting your health and home to covering your car and income. According to the Insurance Information Institute, U.S. insurers collected over $1.4 trillion in net premiums in 2022, which shows just how central insurance has become to modern financial life.

2. How Insurance Works — Step by Step

Understanding how insurance works helps you make smarter choices when comparing policies. Here is the full picture broken down clearly.

Step 1 — You Select a Policy

A policy is your formal contract with the insurance company. It defines what is covered, what is excluded, the limits of coverage, and the rules for filing a claim. You choose a policy based on the risk you want to protect against.

Step 2 — You Pay a Premium

Your premium is the regular payment that keeps your policy active. Premiums can be paid monthly, quarterly, or annually. The cost depends on:

- Your age and health (for life or health insurance)

- Your driving record (for auto insurance)

- The value of what you are insuring

- The level of coverage you choose

- Your location and local risk factors

Step 3 — A Covered Event Occurs

Something unexpected happens — a car crash, a house fire, a medical emergency, or a burglary. This is exactly what your policy is designed for.

Step 4 — You File a Claim

A claim is your formal request for payment under your policy. You submit the claim with supporting documentation — photos, medical records, police reports — depending on the type of incident.

Step 5 — The Insurer Pays Out

If your claim is approved, the insurance company pays the covered amount. They may pay you directly, pay a service provider (like a hospital or repair shop), or pay a third party who suffered a loss because of you.

3. Why Insurance Is Critical in Financial Planning

One of the most important insurance basics to understand is this: insurance is not optional if you are serious about financial stability.

Here is why it sits at the center of sound financial planning:

| Financial Goal | How Insurance Helps |

|---|---|

| Protect your income | Disability insurance replaces income if you cannot work |

| Protect your assets | Home and auto insurance cover property damage or loss |

| Protect your family | Life insurance supports dependents after your death |

| Avoid debt | Health insurance prevents medical bills from becoming debt |

| Build long-term wealth | Insurance stability allows you to invest with confidence |

Medical debt is one of the leading causes of bankruptcy in the United States, according to research from the American Journal of Public Health. A single hospital stay without insurance can cost $30,000 or more. With proper coverage, that same stay might cost you only a few hundred dollars out of pocket.

🔗 Related Reading on Zyqorr.com: Beginner’s Guide to Personal Finance and Risk Management

4. Types of Insurance Explained

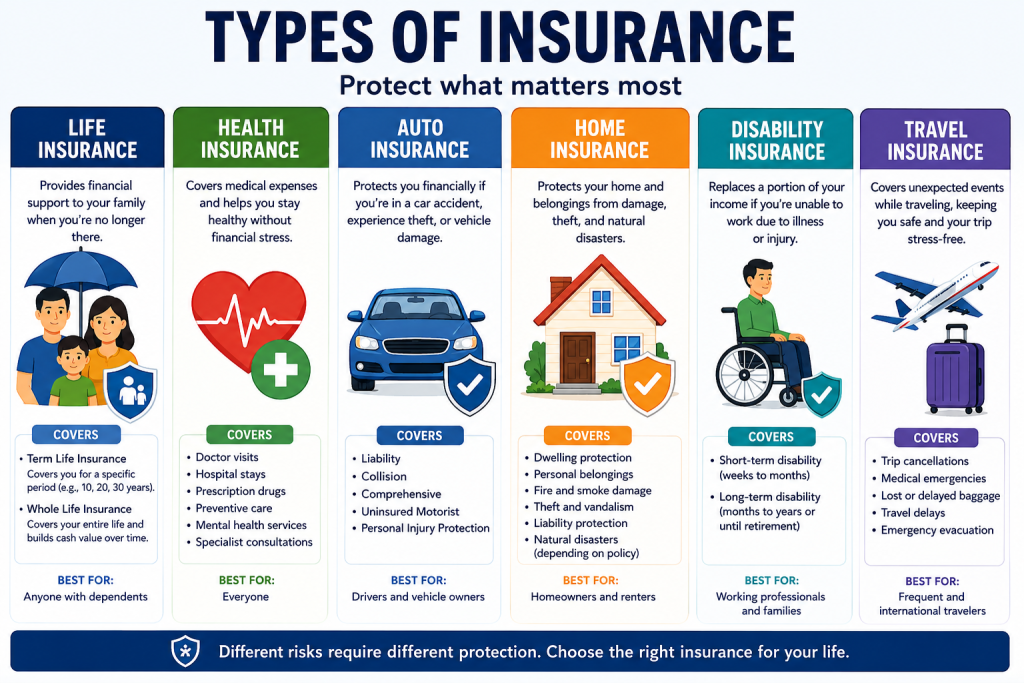

There are many types of insurance, each designed to protect against a specific kind of risk. Here are the most important ones you should know.

Life Insurance

Life insurance pays a lump sum — called a death benefit — to your named beneficiary when you die. It ensures your family can maintain financial stability without your income.

Two main categories:

- Term Life Insurance — Covers you for a fixed period (10, 20, or 30 years). It is affordable and straightforward.

- Whole Life Insurance — Covers your entire life and builds a cash value you can borrow against over time.

Best for: Anyone with dependents — children, a spouse, or aging parents.

Health Insurance

Health insurance covers the cost of medical care, including doctor visits, hospital stays, surgeries, prescription drugs, and preventive care.

Without it, healthcare costs can be financially devastating. The average cost of a three-day hospital stay in the U.S. is approximately $30,000, according to Healthcare.gov.

Key coverages typically included:

- Emergency care

- Preventive checkups and vaccinations

- Specialist consultations

- Prescription medications

- Mental health services

Auto Insurance

Auto insurance protects you financially after a car accident, theft, or vehicle damage. In most countries and U.S. states, a minimum level of auto insurance is required by law.

Common coverage types:

- Liability — Covers damage or injuries you cause to others

- Collision — Covers damage to your car after an accident

- Comprehensive — Covers theft, weather damage, and non-collision events

- Uninsured Motorist — Protects you if the at-fault driver is uninsured

Home Insurance

Home insurance (also known as homeowner’s insurance) protects your home and belongings against fire, theft, vandalism, and certain natural disasters. It also includes liability coverage if someone is injured on your property.

Disability Insurance

Disability insurance replaces a percentage of your income if you are unable to work due to illness or injury.

- Short-term disability — Covers a few weeks to several months

- Long-term disability — Can cover you for years or until retirement

Your income-earning ability is your single greatest financial asset. Protecting it is essential.

Travel Insurance

Travel insurance covers unexpected costs during trips — including medical emergencies abroad, trip cancellations, lost baggage, and travel delays. It is especially valuable for international travel.

Business Insurance

Business insurance protects companies from financial losses due to lawsuits, property damage, employee injuries, and operational disruptions. Common types include general liability, professional liability, and workers’ compensation.

5. Common Insurance Terms You Must Know

One of the most practical insurance basics you can master is understanding the language of insurance. Here are the key terms explained simply.

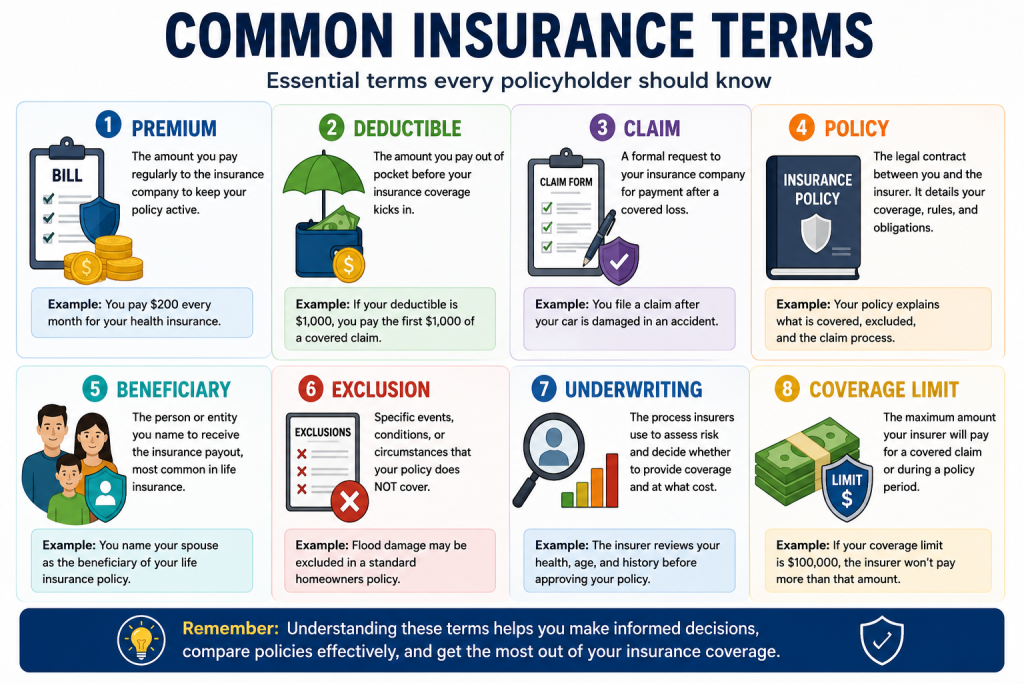

Premium

The regular payment you make to keep your insurance policy active. A higher premium usually means more coverage or a lower deductible.

Claim

A formal request to your insurance company to pay for a covered loss. Always document incidents thoroughly before filing a claim.

Policy

The legal contract between you and the insurer. It details your coverage, exclusions, limits, and the process for filing a claim. Always read it before signing.

Deductible

The amount you pay out of pocket before your insurance coverage kicks in. A $1,000 deductible means you pay the first $1,000 of any covered claim.

Example: If your car repair costs $4,000 and your deductible is $500, you pay $500 and your insurer pays $3,500.

Beneficiary

The person or entity you designate to receive the insurance payout — most commonly used in life insurance policies.

Exclusion

Specific events, conditions, or circumstances that your policy does NOT cover. Reading the exclusions section carefully is critical.

Underwriting

The process the insurance company uses to assess how risky it is to insure you. This determines whether you get coverage and how much your premium will be.

Coverage Limit

The maximum amount an insurer will pay for a covered claim. Always check this before choosing a policy.

6. How to Choose the Right Insurance Policy

Choosing an insurance policy does not have to feel overwhelming. Here is a clear, practical approach.

Step 1 — Identify Your Risks

List what you need to protect — your health, income, home, vehicle, family, or business. Prioritize the most critical risks first.

Step 2 — Set a Realistic Budget

Decide how much you can spend on premiums without straining your monthly finances.

Step 3 — Compare Multiple Quotes

Never buy from the first company you contact. Use comparison tools or work with an independent broker.

🔗 Compare Insurance Quotes: NerdWallet Insurance Comparison Tool

Step 4 — Check Insurer Financial Stability

Look for ratings from AM Best or the Better Business Bureau. A company that cannot pay claims is not worth your premium.

Step 5 — Read the Full Policy

Focus on coverage inclusions, exclusions, limits, and the claims process.

Step 6 — Review Annually

Life changes. Review your policies every year and update them after major life events — marriage, a new child, a home purchase, or a significant income change.

7. Practical Example: Insurance in Real Life

Sarah, 32, a marketing professional, bought a health insurance plan with a $300 monthly premium and a $1,500 deductible. Six months later, she was involved in a cycling accident that required emergency surgery and a two-night hospital stay.

Without insurance, her bill would have been approximately $28,000.

With insurance:

- She paid her $1,500 deductible

- Her insurer covered the remaining $26,500

- Her total out-of-pocket cost: $1,500 + $1,800 in premiums paid so far = $3,300

Her insurance saved her over $24,700 in a single incident.

This is exactly what insurance basics teach us — small, regular payments create a powerful financial shield.

8. Benefits and Advantages of Insurance

- ✅ Protects your savings from being wiped out by a single event

- ✅ Gives you and your family financial security and peace of mind

- ✅ Makes healthcare accessible and affordable

- ✅ Allows you to take calculated risks (like starting a business) knowing you have a safety net

- ✅ Some policies (like whole life insurance) build cash value over time

- ✅ Certain premiums may be tax-deductible depending on your location and policy type

- ✅ Encourages long-term financial planning and goal-setting

9. Risks and Limitations of Insurance

Insurance is powerful, but it is not perfect. Here are the honest limitations you should understand.

- ❌ Premiums are a recurring cost — Even if you never file a claim, you still pay

- ❌ Not everything is covered — Exclusions and limits can leave gaps in protection

- ❌ Claims can be denied — Insurers may reject claims that do not meet policy conditions

- ❌ Underinsurance is common — Many people choose the cheapest plan and discover too late it does not cover enough

- ❌ Complexity — Policy documents can be long, confusing, and filled with legal language

- ❌ Premium increases — Rates can rise over time, especially after filing claims or as you age

Bottom line: Insurance is essential, but informed insurance — knowing exactly what you have and what you do not have — is even better.

10. Step-by-Step Guide to Buying Insurance for the First Time

If you have never bought insurance before, here is exactly where to start.

Step 1: Write down everything you own and everything you are responsible for — your health, car, home, family.

Step 2: Research the types of insurance most relevant to your situation (health and auto are typically the starting point for most people).

Step 3: Get at least three quotes from different insurers for each type of coverage you need.

Step 4: Compare the quotes side by side — look at the premium, deductible, coverage limit, and exclusions together, not just the price.

Step 5: Ask questions. Call the insurer or speak to an independent broker. Ask specifically: “What would NOT be covered in this scenario?”

Step 6: Choose the policy that best balances affordability with adequate coverage.

Step 7: Read the full policy document before signing. Flag anything you do not understand.

Step 8: Set up automatic payments to ensure you never miss a premium and lose coverage.

Step 9: Store a copy of all your policy documents in a safe, accessible place — both digital and physical.

Step 10: Schedule an annual review to reassess your coverage as your life circumstances evolve.

11. Expert Tips for Getting the Best Insurance Coverage

💡 Tip 1 — Bundle Your Policies

Many insurers offer discounts if you buy multiple types of insurance from them — for example, home and auto together. This is called bundling and can reduce premiums by 10–25%.

💡 Tip 2 — Raise Your Deductible to Lower Your Premium

If you have a solid emergency fund, choosing a higher deductible can significantly reduce your monthly premium. Just make sure your emergency fund can cover that deductible if needed.

💡 Tip 3 — Maintain a Good Credit Score

In many states and countries, insurers use credit scores to help set premium rates. A strong credit score can lead to meaningfully lower premiums.

💡 Tip 4 — Review After Every Major Life Change

Marriage, divorce, a new baby, a home purchase, a pay raise — all of these change your insurance needs. Do not wait until renewal to update your policies.

💡 Tip 5 — Work With an Independent Broker

Independent brokers are not tied to a single insurance company, which means they can shop the market on your behalf and find you genuinely competitive options.

💡 Tip 6 — Never Let a Policy Lapse

A gap in coverage — even a short one — can leave you completely exposed. It can also result in higher premiums when you reapply, as some insurers treat a lapse as a risk indicator.

12. Common Insurance Mistakes to Avoid

Even people who understand insurance basics sometimes make costly errors. Here are the most frequent ones.

| Mistake | Why It Is Costly | How to Avoid It |

|---|---|---|

| Choosing price over coverage | Cheap policies often have major gaps | Compare coverage, not just price |

| Not reading exclusions | Claim denials come as a shock | Read the full policy before signing |

| Skipping renters insurance | Your belongings are not covered by your landlord | Get renters insurance — it is inexpensive |

| Ignoring disability insurance | Loss of income is financially devastating | Include disability coverage in your plan |

| Forgetting to update beneficiaries | Payouts can go to the wrong person | Review beneficiaries after every life change |

| Over-insuring low-value items | You pay more than the item is worth | Assess actual replacement value before insuring |

| Missing premium payments | Policy lapses leave you unprotected | Set up automatic payments |

13. FAQs About Insurance Basics

Q1: What is the most important type of insurance for a beginner?

Health insurance and auto insurance are typically the most immediately essential for most adults. Health insurance protects you from catastrophic medical bills, while auto insurance is legally required in most places. If you have dependents, life insurance should be your next priority.

Q2: How is the premium for insurance calculated?

Insurers calculate premiums based on your level of risk. Factors include your age, health status, claims history, credit score (in many regions), location, the type and amount of coverage, and your chosen deductible. The higher the perceived risk, the higher the premium.

Q3: What happens if I miss an insurance premium payment?

Most insurers offer a grace period — typically 10 to 30 days — after a missed payment. If you do not pay within that window, your policy may lapse, meaning you lose all coverage. Some insurers will reinstate a lapsed policy, but this is not guaranteed and may come with higher rates.

Q4: Can I have multiple insurance policies at the same time?

Yes, absolutely. It is both common and advisable to hold several different types of insurance simultaneously — for example, health, auto, life, and home insurance at once. What you want to avoid is overlapping duplicate coverage for the same thing, as that wastes money without providing extra benefit.

Q5: What is the difference between an insurance agent and an insurance broker?

An insurance agent works for a specific insurance company and can only sell that company’s products. An insurance broker works independently and can compare products from multiple companies on your behalf. For the best options, working with a broker is often more beneficial.

Q6: Is insurance worth it if I never make a claim?

Yes. The purpose of insurance is not to guarantee you will use it — it is to guarantee that if something terrible happens, it will not financially destroy you. Think of it as paying for the option to be protected, not a guarantee of a payout. The peace of mind alone has genuine financial and psychological value.

14. Conclusion

Understanding insurance basics is one of the most genuinely valuable things you can do for your financial health.

Here is what you have learned in this guide:

- Insurance is a shared financial safety net that protects you from large, unexpected costs

- It works through risk pooling — many people pay small amounts so that those who suffer losses are covered

- Premiums, claims, policies, deductibles, and beneficiaries are the core terms you must understand before buying any coverage

- The main types — life, health, auto, home, disability, travel, and business insurance — each protect against specific risks

- Choosing the right policy requires assessing your needs, comparing quotes, reading the fine print, and reviewing coverage regularly

- Avoiding common mistakes — like underinsuring, missing payments, or skipping exclusions — can save you from costly surprises

Insurance is not about fear. It is about being smart, prepared, and financially resilient. The people who understand insurance basics are the ones who can face life’s uncertainties without risking everything they have built.

Also Read: How Mutual Funds Work: 7 Essential Steps Every Smart Beginner Must Know

Financial Disclaimer

⚠️ Disclaimer: This content is for educational purposes only and should not be considered financial advice. Insurance needs vary based on individual circumstances, location, and financial goals. Always conduct your own research and consult a licensed insurance professional before making any insurance or financial decisions.

Sources and References

- Insurance Information Institute — Industry Overview

- Healthcare.gov — Health Insurance Basics

- Investopedia — How Insurance Works

- American Journal of Public Health — Medical Debt and Bankruptcy

- NerdWallet — Insurance Comparison Guide

- AM Best — Insurer Financial Ratings

- Better Business Bureau — Insurance Company Reviews

- Zyqorr.com — Financial Education and Trading Guides

{kind=link}