Table of Contents

How mutual funds work is one of the most important concepts every beginner investor should understand before diving into the world of investing. Whether you’re saving for retirement, building an emergency fund, or planning for your children’s education, mutual funds offer a simple yet powerful way to grow your wealth over time.

This comprehensive guide will walk you through everything you need to know about how mutual funds work, from the basic mechanics to advanced strategies. You’ll discover the 7 essential steps that make mutual funds tick, learn about different types available, and understand both the benefits and risks involved. Understanding how mutual funds work will give you the confidence to make informed investment decisions and start your journey toward financial independence.

What Are Mutual Funds and Why Do They Matter?

Understanding how mutual funds work begins with grasping what they actually are. A mutual fund is essentially a pooled investment vehicle where hundreds or thousands of investors combine their money to purchase a diversified portfolio of securities under professional management.

Think of it like this: imagine you and 999 other people each contribute $1,000 to buy a pizza restaurant. Instead of each person owning a tiny piece of one pizza oven, you collectively own the entire restaurant, complete with multiple ovens, ingredients, staff, and everything needed to run a successful business. That’s essentially how mutual funds work in the investment world.

The Core Components

| Component | Description | Importance |

|---|---|---|

| Fund Manager | Professional investment expert | Makes all investment decisions |

| Portfolio | Collection of stocks, bonds, or other securities | Provides diversification |

| Net Asset Value (NAV) | Price per share calculated daily | Determines your investment value |

| Expense Ratio | Annual management fee | Affects your overall returns |

The beauty of understanding how mutual funds work lies in their accessibility. According to the Investment Company Institute, over 100 million Americans own mutual funds, representing more than half of all U.S. households. This popularity stems from their ability to provide professional management and diversification to investors with modest amounts of capital.

When exploring how mutual funds work, it’s important to recognize that these investment vehicles have democratized access to professional money management. Previously, only wealthy individuals could afford portfolio managers and diversified investments. Now, anyone can participate in professionally managed portfolios regardless of their account size.

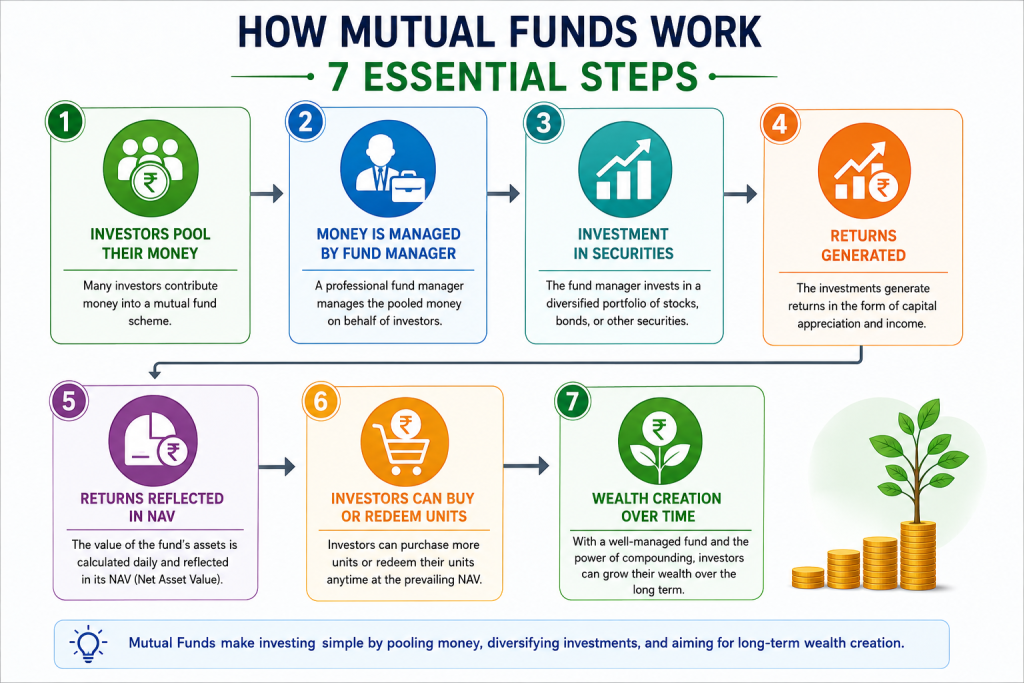

How Mutual Funds Work: The 7 Essential Steps

Understanding how mutual funds work involves following the money from your initial investment through the entire process. Here are the seven essential steps that demonstrate how mutual funds work:

Step 1: Money Pooling and Collection

The first step in understanding how mutual funds work is recognizing how investor money gets pooled together. When you invest in a mutual fund, your money joins a large pool with thousands of other investors. This pooling creates substantial buying power that individual investors could never achieve alone.

For example, if 10,000 investors each contribute $1,000, the fund has $10 million to invest. This significant capital allows the fund to:

- Purchase expensive stocks that individual investors couldn’t afford

- Achieve better diversification across multiple sectors

- Negotiate lower trading costs due to volume

- Access institutional-grade investments

Step 2: Professional Analysis and Research

The second step in how mutual funds work involves professional analysis. The fund management team, led by experienced portfolio managers, conducts extensive research and analysis. They evaluate:

- Market trends and economic indicators

- Company financials including revenue, debt, and growth prospects

- Industry analysis to identify promising sectors

- Risk assessment to maintain appropriate portfolio balance

This professional expertise is what you’re paying for when you invest in actively managed funds. The management team typically has decades of combined experience and access to research tools that individual investors cannot afford.

Step 3: Strategic Asset Allocation

The third component of how mutual funds work is strategic asset allocation. Based on their research and the fund’s investment objectives, managers decide how to allocate the pooled money across different asset classes. This might include:

- Domestic stocks (60%)

- International stocks (20%)

- Bonds (15%)

- Cash equivalents (5%)

The exact allocation depends on the fund’s strategy and current market conditions. Conservative funds might hold more bonds, while aggressive growth funds focus primarily on stocks.

Step 4: Security Selection and Portfolio Construction

Understanding how mutual funds work requires knowledge of security selection. Fund managers use the allocated money to purchase specific securities that align with the fund’s investment strategy. This involves:

- Stock picking based on fundamental analysis

- Bond selection considering credit quality and duration

- Position sizing to manage risk exposure

- Sector diversification to reduce concentration risk

Step 5: Daily Valuation and NAV Calculation

A crucial aspect of how mutual funds work is daily valuation. Every business day after markets close, the fund calculates its Net Asset Value (NAV). The formula is simple:

NAV = (Total Portfolio Value – Fund Expenses) ÷ Number of Outstanding Shares

For instance, if a fund has $100 million in assets, $100,000 in expenses, and 10 million shares outstanding:

NAV = ($100,000,000 – $100,000) ÷ 10,000,000 = $9.99 per share

Step 6: Income Distribution

Another key element of how mutual funds work is income distribution. When the fund’s holdings generate income through dividends or interest payments, this income is distributed to shareholders. Most funds offer two options:

- Cash distributions sent directly to your account

- Automatic reinvestment to purchase additional shares

Step 7: Liquidity and Redemption

The final step in understanding how mutual funds work is liquidity provision. Unlike individual stocks that trade throughout the day, mutual fund shares can only be bought or sold at the day’s closing NAV. When you want to sell your shares, the fund uses cash reserves or sells securities to meet redemption requests.

Types of Mutual Funds Every Beginner Should Know

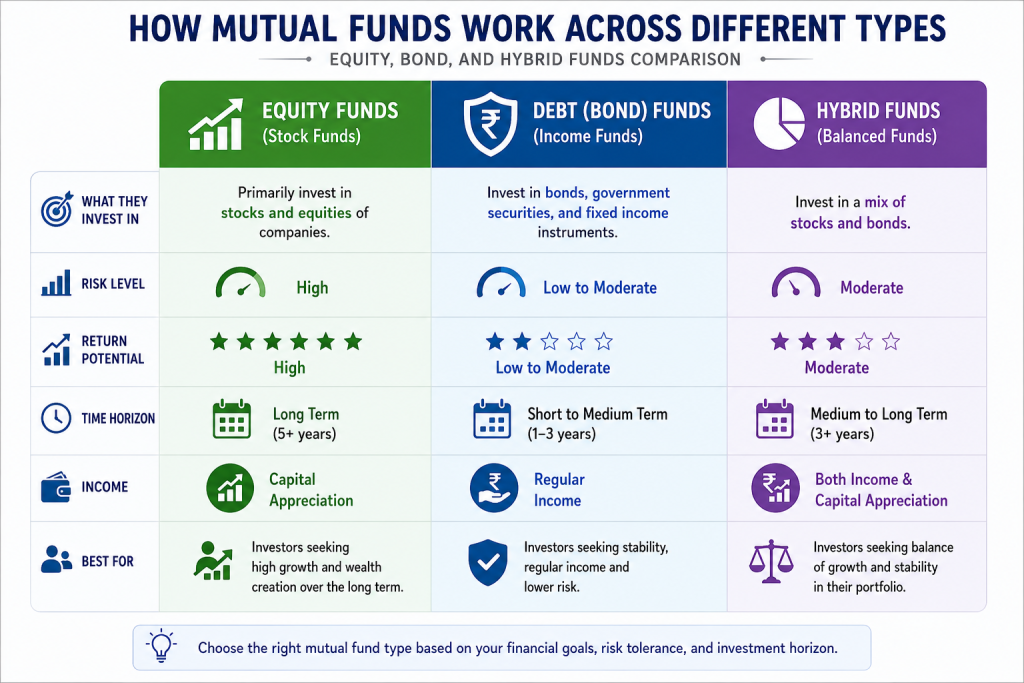

To fully grasp how mutual funds work, you need to understand the different types available. Each type serves specific investment goals and risk tolerances, and knowing how mutual funds work across these categories helps you make better investment decisions.

Equity Funds (Stock Funds)

These funds invest primarily in stocks and are designed for long-term growth. Understanding how mutual funds work in this category reveals they’re further categorized by:

By Market Capitalization:

- Large-cap funds: Invest in established companies like Apple, Microsoft, Amazon

- Mid-cap funds: Focus on medium-sized companies with growth potential

- Small-cap funds: Target smaller companies with high growth possibilities

By Investment Style:

- Growth funds: Seek companies with above-average growth potential

- Value funds: Look for undervalued companies trading below their intrinsic value

- Blend funds: Combine both growth and value strategies

Fixed-Income Funds (Bond Funds)

When learning how mutual funds work with bonds, these funds invest in bonds and other debt securities, providing more stable returns:

- Government bond funds: Invest in U.S. Treasury securities

- Corporate bond funds: Focus on company-issued bonds

- Municipal bond funds: Invest in bonds issued by state and local governments

- High-yield bond funds: Target lower-rated bonds offering higher interest rates

Balanced and Hybrid Funds

Understanding how mutual funds work in this category shows they combine stocks and bonds in a single portfolio:

- Conservative allocation (30% stocks, 70% bonds)

- Moderate allocation (50% stocks, 50% bonds)

- Aggressive allocation (70% stocks, 30% bonds)

Index Funds

How mutual funds work with index investing involves passively tracking market indexes like the S&P 500. According to Morningstar, these funds have gained tremendous popularity due to their low costs and consistent performance.

Specialty Funds

These funds focus on specific sectors or themes, and understanding how mutual funds work in specialized areas includes:

- Technology funds

- Healthcare funds

- Real estate funds (REITs)

- Environmental, Social, and Governance (ESG) funds

For beginners interested in exploring different investment strategies beyond understanding how mutual funds work, check out our comprehensive beginner trading guides for additional insights.

How Mutual Funds Generate Returns for Investors

Understanding how mutual funds work to generate returns is crucial for setting realistic expectations. How mutual funds work to create wealth involves three primary mechanisms:

Capital Appreciation

The first way how mutual funds work to generate returns is through capital appreciation. When the securities in the fund’s portfolio increase in value, the fund’s NAV rises accordingly. For example, if you bought shares at $10 and the NAV grows to $12, you’ve achieved a 20% gain.

Historical Performance Example:

The S&P 500 has averaged approximately 10% annual returns over the past 90 years, according to SEC data. However, this includes both good and bad years, emphasizing the importance of understanding how mutual funds work over long time periods.

Dividend and Interest Income

Another aspect of how mutual funds work involves income generation. Many stocks pay quarterly dividends, while bonds provide regular interest payments. The fund collects this income and distributes it to shareholders based on their ownership percentage.

Example Calculation:

If a fund receives $1 million in dividends and has 10 million shares outstanding, each share receives $0.10 in dividend income.

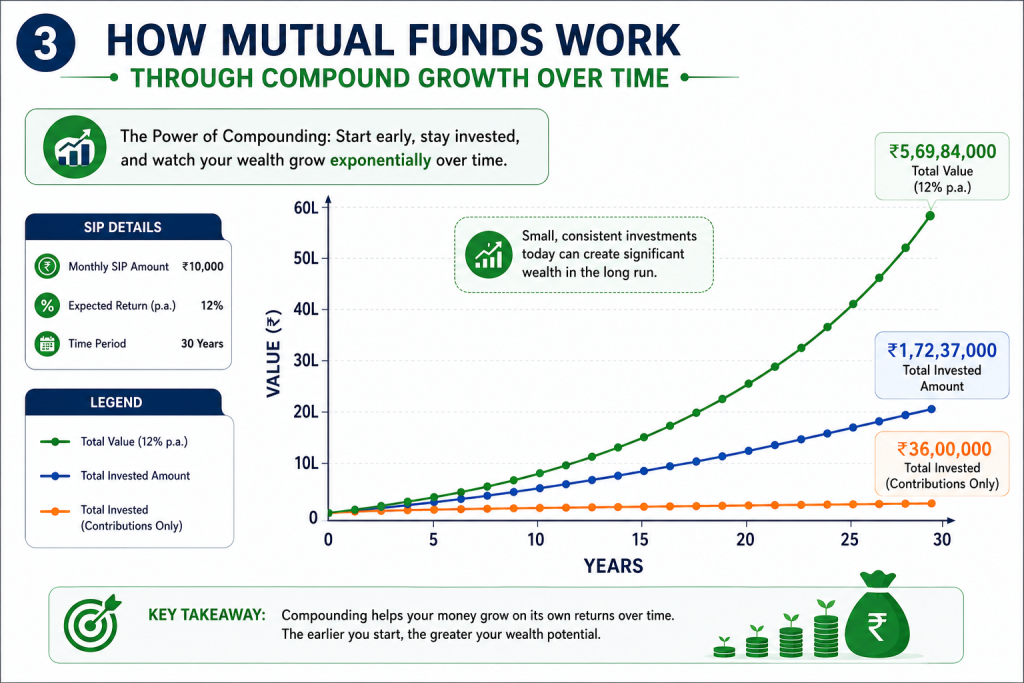

Compound Growth

The most powerful aspect of how mutual funds work is compound growth, where your returns generate additional returns over time.

Compound Growth Example:

- Initial investment: $10,000

- Annual return: 8%

- Time horizon: 30 years

- Final value: $100,627

This demonstrates how mutual funds work through consistent investing and compound growth to multiply your wealth significantly over time.

Key Benefits of Mutual Fund Investing

Understanding how mutual funds work reveals several compelling advantages for individual investors:

Professional Management

One of the key benefits of how mutual funds work is that you gain access to experienced portfolio managers who dedicate their careers to analyzing markets and making investment decisions. This expertise would be impossible for most individual investors to replicate.

Instant Diversification

How mutual funds work to provide diversification is remarkable. Even with a modest investment of $1,000, you can own pieces of hundreds or thousands of different securities. This diversification significantly reduces the risk of losing money due to one company’s poor performance.

Economies of Scale

Understanding how mutual funds work reveals that large mutual funds can:

- Negotiate lower trading commissions

- Access institutional investment opportunities

- Conduct extensive research individual investors cannot afford

Liquidity and Convenience

How mutual funds work in terms of accessibility is impressive. Mutual funds offer excellent liquidity, allowing you to buy or sell shares on any business day. Additionally, most fund companies provide:

- Online account management

- Automatic investment plans

- Tax reporting documents

- Customer service support

Low Minimum Investments

Another benefit of how mutual funds work is accessibility. Many funds require minimum investments of just $100-$1,000, making them accessible to beginning investors. Some funds waive minimums entirely for automatic investment plans.

Regulatory Protection

Understanding how mutual funds work includes knowing they’re heavily regulated by the Securities and Exchange Commission (SEC), providing important investor protections including:

- Required disclosure of holdings and performance

- Independent oversight by fund boards

- Strict rules governing fund operations

- Insurance protection through SIPC

Understanding the Risks and Limitations

While learning how mutual funds work, it’s essential to understand the associated risks and limitations:

Market Risk

The most significant risk when understanding how mutual funds work is that your investment value can decline when markets fall. During the 2008 financial crisis, many equity mutual funds lost 30-40% of their value.

Risk Mitigation Strategies:

- Diversify across multiple fund types

- Maintain a long-term investment horizon

- Consider dollar-cost averaging

- Regularly rebalance your portfolio

Interest Rate Risk

How mutual funds work with bonds shows they’re particularly sensitive to interest rate changes. When rates rise, existing bond values fall, negatively impacting fund performance.

Credit Risk

Understanding how mutual funds work includes recognizing that if companies or governments that issued bonds in the fund’s portfolio experience financial difficulties, the fund’s value may decline.

Inflation Risk

Another aspect of how mutual funds work is that if your returns don’t keep pace with inflation, your purchasing power decreases over time, even if your account value grows.

Management Risk

How mutual funds work depends heavily on fund managers, and poor decisions by these managers can negatively impact performance. This is why researching a fund’s management team and track record is crucial.

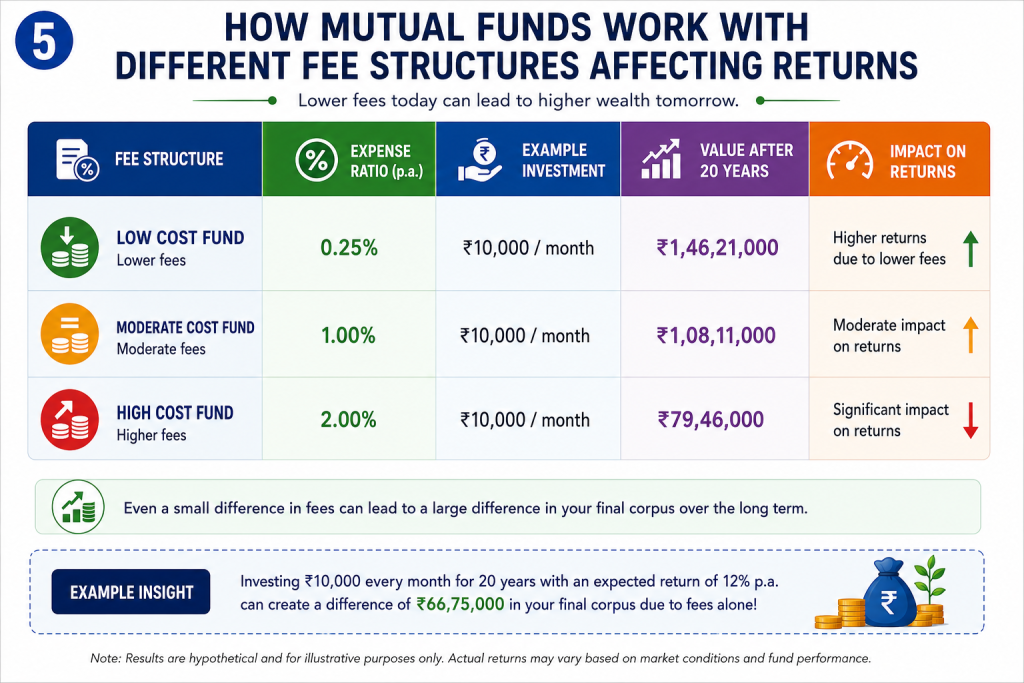

Expense Risk

Understanding how mutual funds work includes recognizing that high fees can significantly erode returns over time. A 1% difference in annual fees can cost tens of thousands of dollars over a 30-year investment period.

Fee Comparison Example:

- Fund A: $10,000 initial investment, 8% annual return, 0.5% expense ratio = $66,208 after 25 years

- Fund B: $10,000 initial investment, 8% annual return, 1.5% expense ratio = $54,274 after 25 years

- Difference: $11,934

For more detailed information about managing investment risks beyond understanding how mutual funds work, explore our risk management articles.

Step-by-Step Guide to Start Investing

Now that you understand how mutual funds work, here’s a practical guide to begin your investment journey:

Step 1: Define Your Investment Goals

Before selecting any mutual fund, and regardless of how mutual funds work, clearly define what you’re investing for:

- Retirement (long-term, growth-focused)

- House down payment (medium-term, moderate risk)

- Emergency fund (short-term, capital preservation)

- Children’s education (medium to long-term, balanced approach)

Step 2: Assess Your Risk Tolerance

Understanding how mutual funds work for different risk levels helps you choose appropriately:

| Factor | Conservative | Moderate | Aggressive |

|---|---|---|---|

| Age | 50+ | 30-50 | Under 30 |

| Time Horizon | <5 years | 5-15 years | 15+ years |

| Income Stability | Fixed income | Stable job | Growing career |

| Emotional Comfort | Dislikes volatility | Tolerates some ups/downs | Comfortable with volatility |

Step 3: Determine Your Asset Allocation

A common rule when understanding how mutual funds work is to subtract your age from 110 to determine your stock allocation percentage. For example:

- Age 30: 80% stocks, 20% bonds

- Age 50: 60% stocks, 40% bonds

- Age 70: 40% stocks, 60% bonds

Step 4: Research and Select Funds

When evaluating how mutual funds work for your portfolio, consider these key factors:

Performance Metrics:

- Past performance (3, 5, and 10-year returns)

- Consistency of performance across market cycles

- Benchmark comparison against relevant indexes

Fund Characteristics:

- Expense ratio (aim for <1% for actively managed funds)

- Fund size (assets under management)

- Manager tenure and track record

- Investment strategy alignment with your goals

Research Resources:

- Morningstar.com for comprehensive fund analysis

- Fund company websites for prospectuses and fact sheets

- SEC EDGAR database for regulatory filings

Step 5: Choose Your Investment Platform

Understanding how mutual funds work includes knowing where to buy them:

Direct from Fund Companies:

- Pros: Often lower or no sales charges, direct customer service

- Cons: Limited fund selection from one company

Discount Brokers:

- Pros: Wide fund selection, competitive pricing, research tools

- Cons: May charge transaction fees for some funds

Full-Service Brokers:

- Pros: Personal advice, comprehensive financial planning

- Cons: Higher fees, potential conflicts of interest

Employer-Sponsored Plans:

- Pros: Employer matching, payroll deduction convenience

- Cons: Limited fund choices

Step 6: Start with Systematic Investing

Regardless of how mutual funds work, consider beginning with a systematic investment plan (SIP) that automatically invests a fixed amount regularly. Benefits include:

- Dollar-cost averaging reduces timing risk

- Discipline removes emotional decision-making

- Convenience automates the investment process

- Flexibility to start with small amounts

Step 7: Monitor and Rebalance

Understanding how mutual funds work long-term requires regular portfolio review. Examine your portfolio at least annually and rebalance when allocations drift significantly from targets. Rebalancing forces you to sell high-performing assets and buy underperforming ones, maintaining your desired risk level.

Also Read: 7 Essential Mutual Funds Facts Every Smart Investor Must Know

Expert Tips for Successful Mutual Fund Investing

After understanding how mutual funds work, these expert strategies can help maximize your success:

Focus on Low-Cost Funds

Research consistently shows that understanding how mutual funds work regarding fees is crucial, as low-cost funds outperform high-cost funds over time. According to Morningstar research, expense ratios are one of the best predictors of future fund performance.

Diversify Across Fund Types

Don’t put all your money in one fund or fund type, regardless of how mutual funds work. A well-diversified portfolio might include:

- 40% U.S. stock funds

- 20% international stock funds

- 30% bond funds

- 10% alternative investments

Consider Index Funds

For many investors learning how mutual funds work, low-cost index funds provide better long-term returns than actively managed funds. They offer:

- Lower expense ratios (often <0.20%)

- Broad market exposure

- Consistent performance relative to benchmarks

- No manager risk

Invest Regularly

Understanding how mutual funds work with consistent investing shows that regular contributions through market ups and downs help smooth volatility and take advantage of dollar-cost averaging. Even investing $100 monthly can build substantial wealth over time.

Stay the Course

Regardless of how mutual funds work, avoid making emotional decisions based on short-term market movements. Successful investing requires patience and discipline. Historical data shows that investors who try to time the market typically underperform those who stay invested.

Maximize Tax Efficiency

Understanding how mutual funds work in tax-advantaged accounts is important. Consider holding mutual funds in:

- 401(k) or 403(b) for retirement savings

- Traditional or Roth IRAs for additional retirement savings

- 529 plans for education expenses

- HSAs for healthcare costs (triple tax advantage)

Common Mistakes Every Beginner Should Avoid

Understanding how mutual funds work also means knowing what not to do:

Chasing Performance

Don’t invest in funds solely based on recent strong performance, regardless of how mutual funds work. Studies show that yesterday’s winners often become tomorrow’s underperformers.

Better Approach: Focus on consistent long-term performance and low costs rather than short-term results.

Ignoring Fees

A seemingly small difference in expense ratios can cost you thousands of dollars over time, no matter how mutual funds work. Always compare fees when selecting between similar funds.

Over-Diversification

While understanding how mutual funds work shows diversification is important, owning too many similar funds provides no additional benefit and may increase costs. Focus on complementary funds rather than overlapping ones.

Emotional Trading

Don’t panic and sell during market downturns or get overexcited during bull markets, regardless of how mutual funds work. Emotional decisions typically result in buying high and selling low.

Neglecting Rebalancing

Failing to rebalance your portfolio allows your asset allocation to drift, potentially increasing risk beyond your comfort level, no matter how mutual funds work.

Focusing Only on Past Performance

While historical performance provides useful information when understanding how mutual funds work, it doesn’t guarantee future results. Consider all factors including fees, strategy, and management quality.

Waiting for the “Perfect” Time

There’s never a perfect time to start investing, regardless of how mutual funds work. Begin as soon as possible to maximize the benefits of compound growth.

For additional insights on avoiding common investment pitfalls beyond understanding how mutual funds work, check out our trading psychology posts.

Frequently Asked Questions

How much money do I need to start investing in mutual funds?

Understanding how mutual funds work regarding minimums shows that many mutual funds have minimum investments ranging from $100 to $3,000, though some require no minimum if you set up automatic monthly investments. Start with whatever amount you can afford and increase it over time.

How often should I check my mutual fund performance?

When learning how mutual funds work, checking quarterly or annually is sufficient for long-term investors. Monitoring too frequently can lead to emotional decisions that hurt long-term returns. Focus on your long-term goals rather than short-term fluctuations.

What’s the difference between load and no-load mutual funds?

Understanding how mutual funds work with fees shows that load funds charge sales commissions (typically 3-6%) when you buy or sell shares. No-load funds don’t charge these fees. Generally, no-load funds are preferable because the sales charges reduce your investment returns.

Can I lose all my money in mutual funds?

While theoretically possible, it’s extremely unlikely with diversified mutual funds when you understand how mutual funds work. However, you can lose money, especially in the short term during market downturns. This is why having a long-term investment horizon is important.

Should I invest in actively managed funds or index funds?

Both have merits when understanding how mutual funds work. Index funds typically offer lower costs and consistent market returns, while actively managed funds aim to beat the market but charge higher fees. Many experts recommend starting with low-cost index funds.

How are mutual funds taxed?

Understanding how mutual funds work regarding taxes shows they’re subject to taxes on dividends, capital gains distributions, and capital gains when you sell shares. The tax treatment depends on how long you hold the investment and your tax bracket. Consider holding funds in tax-advantaged accounts when possible.

Conclusion

Understanding how mutual funds work is fundamental to building long-term wealth through investing. These powerful investment vehicles offer professional management, diversification, and accessibility that make them ideal for both beginning and experienced investors.

The key takeaways from learning how mutual funds work include:

- Mutual funds pool money from many investors to create diversified portfolios under professional management

- They generate returns through capital appreciation, dividends, and compound growth

- Different fund types serve various investment goals and risk tolerances

- Success requires focusing on low costs, regular investing, and long-term patience

- Avoiding common mistakes like chasing performance and emotional trading is crucial

Remember that understanding how mutual funds work is just the beginning – successful investing is a marathon, not a sprint. Start with clear goals, choose appropriate funds, invest regularly, and stay disciplined. The power of compound growth will work in your favor over time.

Ready to begin your mutual fund investment journey? Start by defining your goals and exploring the educational resources available at Zyqorr.com. Our comprehensive guides and expert insights can help you make informed investment decisions and build the financial future you deserve.

Take action today – your future self will thank you for starting now rather than waiting for the “perfect” moment that never comes.

Financial Disclaimer

This content is for educational purposes only and should not be considered financial advice. Always conduct your own research before making financial decisions. Consider consulting with a qualified financial advisor who can provide personalized advice based on your individual circumstances, goals, and risk tolerance.

{kind=link}