Table of Contents

Introduction

Mutual funds represent one of the most accessible and effective investment vehicles for building long-term wealth, yet many investors still find themselves confused about the basics. Whether you’re a complete beginner or someone looking to refine your investment strategy, understanding how mutual funds work can transform your financial future. This comprehensive guide will walk you through everything you need to know about mutual funds, from fundamental concepts to advanced investment strategies that seasoned investors use to maximize their returns.

What Are Mutual Funds: The Foundation

Mutual funds are professionally managed investment vehicles that pool money from thousands of individual investors to purchase a diversified portfolio of stocks, bonds, or other securities. Think of mutual funds as a large basket where many people contribute money, and a professional fund manager uses this collective investment to buy various assets that individual investors might not afford or have the expertise to select.

When you invest in mutual funds, you purchase shares of the fund, and each share represents a proportional ownership of the fund’s holdings. The value of your investment fluctuates based on the performance of the underlying securities in the portfolio.

Core Components of Investment Funds

Portfolio Management: Professional fund managers with extensive market experience make investment decisions on behalf of all shareholders.

Diversification: Your investment is automatically spread across multiple securities, reducing the risk associated with investing in individual stocks or bonds.

Net Asset Value (NAV): The price per share of these investment vehicles, calculated daily by dividing the total value of all securities minus liabilities by the number of outstanding shares.

Liquidity: Most investment options offer daily liquidity, meaning you can buy or sell shares on any business day at the current NAV.

How Mutual Funds Work Behind the Scenes

Understanding the mechanics of mutual funds helps investors make informed decisions. The process begins when the fund company establishes an investment objective, such as growth, income, or capital preservation. Professional fund managers then research and select securities that align with these objectives.

The Investment Process

Research and Analysis: Fund managers conduct thorough research using fundamental analysis, technical analysis, and economic forecasts to identify promising investment opportunities.

Portfolio Construction: Based on their research, managers construct a diversified portfolio that balances risk and return potential according to the fund’s stated objectives.

Ongoing Management: Managers continuously monitor the portfolio, making buy and sell decisions based on changing market conditions, company fundamentals, and economic factors.

Performance Monitoring: The fund’s performance is tracked against relevant benchmarks and peer groups to ensure it meets investor expectations.

Daily Operations

Every business day, investment vehicles calculate their NAV after the market closes. When investors place buy or sell orders, these transactions are processed at the end-of-day NAV. This differs from stocks, which trade throughout the day at fluctuating prices.

The fund company handles all administrative tasks, including dividend distributions, capital gains distributions, and providing regular statements to shareholders.

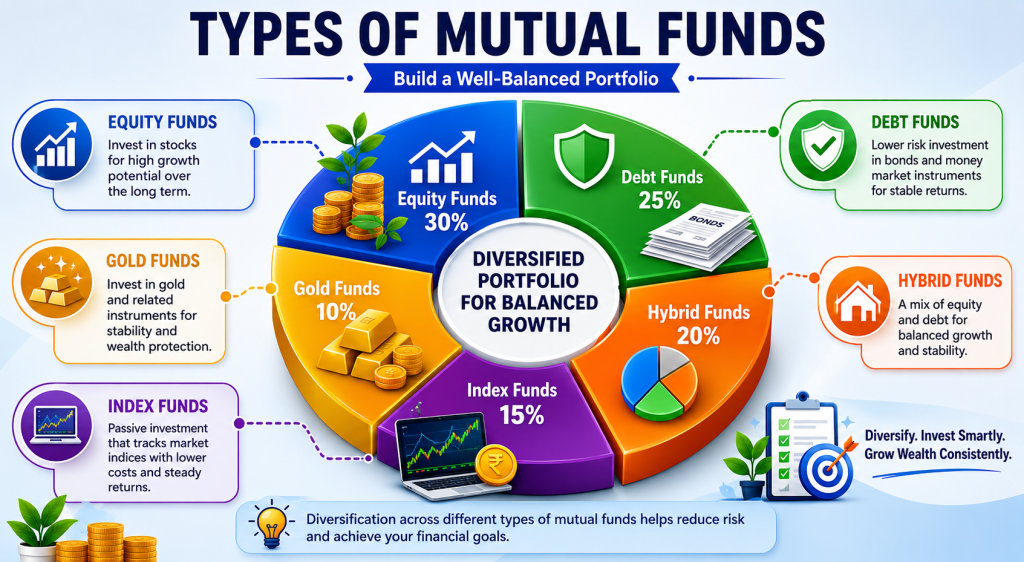

Types of Mutual Funds for Different Investment Goals

Mutual funds come in various categories, each designed to meet specific investment objectives and risk tolerances. Understanding these categories helps investors select funds that align with their financial goals.

Equity Investment Options

Large-Cap Funds: Invest primarily in large, established companies with market capitalizations typically exceeding $10 billion. These mutual funds offer relatively stable returns with lower volatility compared to other equity categories.

Mid-Cap Funds: Focus on medium-sized companies with market caps between $2-10 billion. These funds offer higher growth potential but with increased volatility.

Small-Cap Funds: Invest in smaller companies with market caps under $2 billion. While offering the highest growth potential, these options also carry the highest risk among equity categories.

Sector Funds: Concentrate investments in specific industries such as technology, healthcare, or energy. These specialized vehicles allow investors to capitalize on particular market segments.

Fixed-Income Investment Options

Government Bond Funds: Invest in government securities, offering lower risk and steady income. These options are ideal for conservative investors seeking capital preservation.

Corporate Bond Funds: Focus on bonds issued by corporations, typically offering higher yields than government bonds but with increased credit risk.

High-Yield Bond Funds: Invest in lower-rated bonds that offer higher interest rates to compensate for increased default risk.

Hybrid Investment Options

Balanced Funds: Maintain a predetermined allocation between stocks and bonds, typically 60% equity and 40% fixed income. These mutual funds provide built-in diversification across asset classes.

Target-Date Funds: Automatically adjust asset allocation based on the investor’s expected retirement date, becoming more conservative as the target date approaches.

Index Investment Options

Broad Market Index Funds: Track major market indices like the S&P 500, providing market returns at low cost.

Sector Index Funds: Track specific sector indices, allowing investors to gain exposure to particular market segments without active management fees.

Key Benefits of Investing in Mutual Funds

Mutual funds offer numerous advantages that make them attractive to investors across all experience levels and financial situations.

Professional Management

One of the primary benefits of mutual funds is access to professional investment management. Fund managers possess extensive education, experience, and resources that individual investors typically lack. They conduct thorough research, analyze market trends, and make informed investment decisions on behalf of shareholders.

Professional managers also have access to institutional-quality research, advanced analytical tools, and direct communication with company management teams. This level of expertise would be extremely difficult and expensive for individual investors to replicate.

Instant Diversification

These investment vehicles provide immediate diversification across numerous securities, industries, and sometimes geographic regions. A single fund might hold hundreds or even thousands of different investments, spreading risk across multiple positions.

This diversification helps reduce the impact of poor performance from any single investment on the overall portfolio. While individual stocks might experience significant volatility, these pooled investments tend to have more stable returns due to their diversified nature.

Cost Efficiency

Investing in these vehicles is generally more cost-effective than building a diversified portfolio of individual securities. The pooled nature allows investors to benefit from economies of scale, reducing transaction costs and management fees on a per-investor basis.

Additionally, these options eliminate the need to research and select individual securities, saving investors significant time and effort while providing professional management at a reasonable cost.

Flexibility and Convenience

These investment options offer excellent flexibility through features like systematic investment plans (SIPs), automatic dividend reinvestment, and easy portfolio rebalancing. Investors can start with relatively small amounts and add to their investments regularly.

Most fund companies provide online platforms that make it easy to monitor investments, make changes, and access important documents. This convenience factor makes these vehicles particularly attractive to busy professionals who lack time for active portfolio management.

Understanding Mutual Fund Fees and Expenses

All mutual funds charge fees to cover management costs, but understanding these fees helps investors make informed decisions and maximize returns.

Expense Ratios

The expense ratio represents the annual fee charged by these investment vehicles, expressed as a percentage of your investment. This fee covers management costs, administrative expenses, and other operational costs.

Actively Managed Options: Typically charge expense ratios between 0.5% to 2.0% annually, with equity funds generally charging more than bond funds.

Index Options: Usually have much lower expense ratios, often between 0.05% to 0.50%, because they require less active management.

Impact on Returns: Over time, expense ratios significantly impact investment returns. A difference of just 1% in annual fees can reduce portfolio value by hundreds of thousands of dollars over a 30-year investment period.

Load Fees

Some investment vehicles charge load fees, which are sales commissions paid when buying or selling fund shares.

Front-End Loads: Charged when purchasing fund shares, typically ranging from 3% to 5.75% of the investment amount.

Back-End Loads: Charged when selling fund shares, usually declining over time if you hold the investment for several years.

No-Load Options: Many mutual funds don’t charge load fees, making them more cost-effective for investors.

Other Fees to Consider

12b-1 Fees: Annual marketing and distribution fees that some investment vehicles charge, typically 0.25% to 1.00% of assets.

Redemption Fees: Short-term trading fees charged when selling fund shares within a specific period, usually 30 to 90 days.

Account Maintenance Fees: Some fund companies charge annual account fees for small balances, typically $10 to $50 per year.

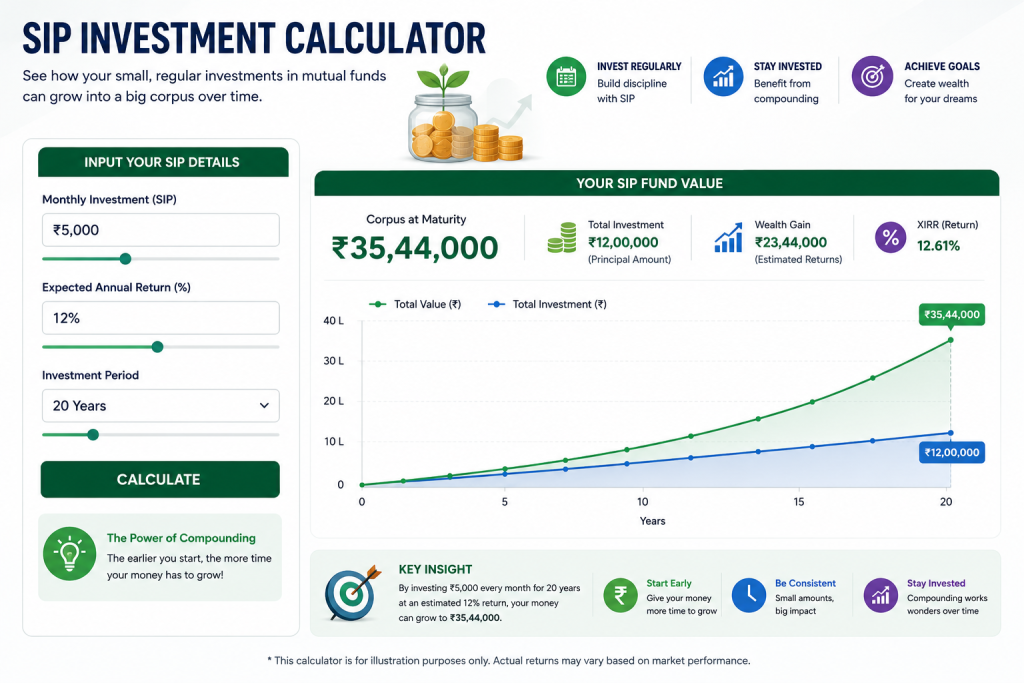

SIP Investment Strategy for Long-term Success

Systematic Investment Plans (SIP) represent one of the most effective strategies for investing in mutual funds, particularly for long-term wealth building.

How SIP Works with Investment Vehicles

SIP involves investing a fixed amount in these pooled investments at regular intervals, typically monthly. This approach offers several advantages over lump-sum investing, especially for average investors who want to build wealth gradually.

Rupee Cost Averaging: When markets are high, your fixed SIP amount buys fewer fund units. When markets decline, the same amount purchases more units. Over time, this averaging effect reduces the average cost per unit.

Disciplined Investing: SIP creates a systematic approach to investing, helping investors overcome emotional decision-making that often leads to poor timing.

Compounding Benefits: Regular investments through SIP harness the power of compounding, where returns generate additional returns over time.

Optimizing Your SIP Strategy

Start Early: The earlier you begin SIP investments, the more time your money has to grow through compounding.

Increase Gradually: Consider increasing your SIP amount annually as your income grows, maximizing the wealth-building potential.

Stay Consistent: Continue your SIP even during market downturns, as these periods often provide the best buying opportunities.

Choose Appropriate Options: Select mutual funds that align with your investment timeline and risk tolerance for optimal SIP results.

How to Choose the Right Mutual Funds

Selecting appropriate mutual funds requires careful analysis of multiple factors to ensure alignment with your investment objectives and risk profile.

Performance Analysis

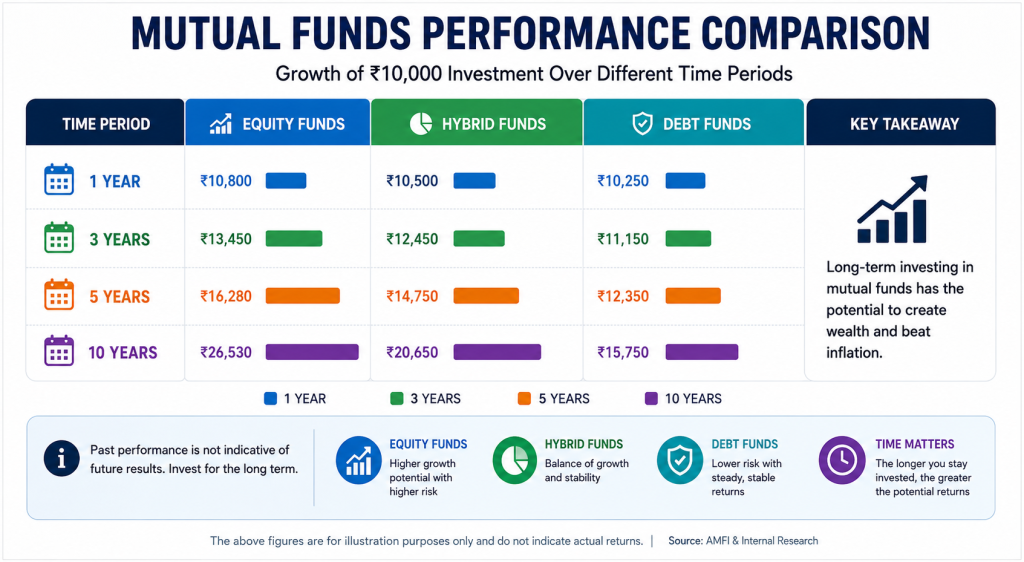

Historical Returns: Examine how these vehicles have performed over various time periods (1, 3, 5, and 10+ years) to understand consistency and long-term trends.

Benchmark Comparison: Compare fund performance against relevant benchmarks to determine if these options are adding value through active management.

Risk-Adjusted Returns: Consider metrics like Sharpe ratio and standard deviation to evaluate how these vehicles balance returns against risk.

Consistency Metrics: Look for mutual funds that demonstrate consistent performance across different market cycles rather than those with spectacular short-term returns.

Fund Management Quality

Manager Experience: Research the fund manager’s track record, investment philosophy, and tenure with current investment vehicles.

Investment Process: Understand how managers select investments and whether their approach aligns with stated objectives.

Team Stability: Consider whether these options have experienced significant management changes that might affect future performance.

Portfolio Characteristics

Holdings Analysis: Examine what securities these vehicles own to understand diversification, concentration risk, and investment style.

Turnover Ratio: High turnover can indicate frequent trading that may increase costs and tax implications.

Asset Size: Very large or very small funds may face unique challenges that affect performance potential.

Step-by-Step Guide to Start Investing

Beginning your mutual funds investment journey requires careful planning and systematic execution.

Step 1: Define Investment Objectives

Goal Setting: Clearly define what you want to achieve through investing, such as retirement planning, children’s education, or wealth accumulation.

Timeline Determination: Establish when you’ll need access to your money, as this affects which types of investment vehicles are most appropriate.

Risk Assessment: Honestly evaluate your risk tolerance to select options that match your comfort level with market volatility.

Step 2: Research and Selection

Fund Screening: Use online tools and resources to screen investment options based on your criteria, including investment style, performance, and fees.

Due Diligence: Read fund prospectuses and annual reports to understand investment strategies and risks of potential mutual funds.

Professional Consultation: Consider speaking with financial advisors who can provide personalized recommendations based on your situation.

Step 3: Account Opening and Investment

Platform Selection: Choose between investing directly with fund companies, through online brokers, or via financial advisors for your purchases.

Documentation: Complete required paperwork, including account applications and risk assessment questionnaires.

Initial Investment: Make your first investment in selected options, keeping in mind minimum investment requirements.

Step 4: Ongoing Management

Regular Monitoring: Review your performance periodically, but avoid making frequent changes based on short-term market movements.

Rebalancing: Adjust your portfolio allocation periodically to maintain desired asset allocation across different vehicles.

Performance Review: Conduct annual reviews to ensure your mutual funds continue meeting your objectives and performance expectations.

Also Read: What is Trading Psychology? The Complete Guide to Mastering Your Mind in Trading

Expert Tips for Successful Mutual Fund Investing

Experienced investors have developed proven strategies for maximizing returns and minimizing risks when investing in mutual funds.

Diversification Strategies

Asset Class Diversification: Spread investments across different types of vehicles, including equity, fixed-income, and international options.

Style Diversification: Combine investment options with different styles, such as growth and value, to reduce style-specific risks.

Geographic Diversification: Consider international mutual funds to reduce dependence on domestic market performance.

Timing and Market Considerations

Long-term Perspective: Successful investing requires patience and a long-term outlook, typically 5+ years for equity funds.

Market Timing Avoidance: Avoid trying to time market entries and exits, as this strategy rarely succeeds.

Regular Investment: Use SIP to invest regularly, taking advantage of market volatility through rupee cost averaging.

Tax Optimization

Tax-Efficient Options: Choose vehicles with low turnover ratios to minimize taxable capital gains distributions.

Asset Location: Hold tax-inefficient options in tax-advantaged accounts when possible to optimize after-tax returns.

Harvest Losses: Consider tax-loss harvesting strategies to offset capital gains in taxable accounts.

Common Mistakes That Cost Investors Money

Understanding common pitfalls helps investors avoid costly errors when investing in mutual funds.

Performance Chasing

Many investors make the mistake of selecting investment options based solely on recent strong performance. This often leads to buying high and selling low, as yesterday’s top-performing funds may become tomorrow’s underperformers.

Solution: Focus on consistent long-term performance rather than short-term results when selecting investment vehicles.

Excessive Trading

Frequent buying and selling based on market news or short-term performance typically reduces returns due to transaction costs and poor timing.

Solution: Develop a long-term investment strategy and stick with it, making changes only when fundamental circumstances change.

Inadequate Diversification

Some investors put too much money into similar options or concentrate heavily in one asset class, failing to achieve proper diversification.

Solution: Spread investments across different types of mutual funds and asset classes based on your risk tolerance and investment objectives.

Ignoring Fees

High fees can significantly erode returns over time, yet many investors fail to consider expense ratios when selecting investment options.

Solution: Compare expense ratios and choose low-cost options when similar alternatives are available, particularly for index funds.

Emotional Decision Making

Market volatility often triggers emotional responses that lead to poor investment decisions.

Solution: Stick to your investment plan and avoid making impulsive decisions based on short-term market movements.

Tax Implications and Optimization Strategies

Understanding the tax implications of mutual funds investing helps maximize after-tax returns.

Capital Gains Treatment

Short-term Capital Gains: Profits from investments held less than one year are taxed as ordinary income at your marginal tax rate.

Long-term Capital Gains: Profits from investments held more than one year typically receive preferential tax treatment with lower rates.

Tax-Loss Harvesting: Selling investments at a loss can offset gains from other holdings, reducing overall tax liability.

Distribution Taxation

Dividend Distributions: Investment vehicles may distribute dividends from underlying holdings, which are typically taxed as ordinary income or qualified dividends.

Capital Gains Distributions: When funds sell securities at a profit, they distribute capital gains to shareholders, creating taxable events.

Tax-Efficient Strategies

Index Options: These vehicles typically generate fewer taxable distributions due to their buy-and-hold approach.

Tax-Managed Options: Some mutual funds specifically focus on minimizing taxable distributions for investors in high tax brackets.

Asset Location: Hold tax-inefficient vehicles in retirement accounts and tax-efficient funds in taxable accounts.

Risks and Limitations You Should Know

While mutual funds offer many benefits, investors should understand associated risks and limitations.

Market Risk

Investment vehicles are subject to market risk, meaning their value can decline due to overall market conditions, economic factors, or geopolitical events. Even well-diversified options cannot completely eliminate market risk.

Management Risk

Active vehicles depend on manager skill and decision-making. Poor management decisions can result in underperformance relative to benchmarks or peer funds.

Liquidity Limitations

While most mutual funds offer daily liquidity, some specialized funds may have restrictions on redemptions or may invest in less liquid securities.

Style Drift

Some vehicles may gradually shift their investment style or strategy over time, potentially no longer matching investor expectations or needs.

Concentration Risk

Sector-specific or geographically concentrated options may be more volatile than broadly diversified funds due to concentration risk.

FAQs

Q: What is the minimum amount needed to invest in mutual funds?

A: Most mutual funds have minimum requirements ranging from $100 to $3,000 for initial investments. However, many fund companies offer lower minimums for systematic investment plans (SIPs), sometimes as low as $25-50 per month. Some online brokers also offer fractional investing with no minimums.

Q: How often should I review my mutual funds investments?

A: Review your portfolio quarterly or semi-annually to monitor performance and ensure alignment with your goals. However, avoid making frequent changes based on short-term performance. Annual reviews are typically sufficient for long-term investors unless major life changes affect your investment objectives.

Q: Can I lose money investing in mutual funds?

A: Yes, mutual funds can lose value, and you can lose money, especially in the short term. However, historically, well-diversified equity options have provided positive returns over long periods (10+ years). The risk of loss decreases with longer investment horizons and proper diversification across different types of vehicles.

Q: What’s the difference between actively managed and passively managed mutual funds?

A: Actively managed mutual funds employ professional managers who research and select investments to outperform market benchmarks. Passively managed options (index funds) track specific market indices. Active funds typically charge higher fees but aim for superior returns, while passive funds offer market returns at lower costs.

Q: How are mutual funds different from ETFs?

A: Mutual funds are priced once daily after market close and can only be bought or sold at that price. ETFs trade throughout the day like stocks at market prices. These pooled investments often have minimum investment requirements, while ETFs can be purchased in any amount. Both offer professional management and diversification benefits.

Q: When is the best time to invest in mutual funds?

A: The best time to invest in mutual funds is as soon as possible if you have a long-term investment horizon. Time in the market is generally more important than timing the market. Starting early allows you to benefit from compounding returns and ride out short-term market volatility. SIP investing can help smooth out market timing concerns.

Conclusion

Mutual funds represent one of the most accessible and effective ways to build long-term wealth through professional investment management and diversification. Throughout this comprehensive guide, we’ve explored the fundamental concepts, various types, benefits, and strategies that make these investment vehicles an excellent choice for investors at all levels.

The key to success with mutual funds lies in understanding your investment objectives, selecting appropriate funds that match your risk tolerance and timeline, and maintaining a disciplined long-term approach. Whether you choose equity funds for growth, bond funds for stability, or hybrid options for balanced exposure, these vehicles provide the professional management and diversification that individual investors need.

Remember that investing in mutual funds is a marathon, not a sprint. Start with a systematic investment plan, stay consistent through market ups and downs, and let the power of compounding work in your favor. With proper planning and patience, these investment options can help you achieve your financial goals and build lasting wealth.

Ready to begin your mutual funds investment journey? Explore our comprehensive trading guides and investment strategies at Zyqorr.com to continue your financial education and make informed investment decisions.

Financial Disclaimer

This content is for educational purposes only and should not be considered financial advice. Mutual funds investing involves risk, including potential loss of principal. Past performance does not guarantee future results. Always conduct your own research and consider consulting with a qualified financial advisor before making investment decisions regarding any financial products.

{kind=link}