Table of Contents

Introduction

Life insurance is one of the most important financial decisions you will ever make — yet most people in India either delay buying it, buy the wrong type, or buy far too little cover.

Think about this for a moment. If you are the primary earner in your family and something unexpected happens to you tomorrow, what happens to your family’s finances? Who pays the home loan EMI? Who funds your child’s education? Who takes care of your aging parents?

These are uncomfortable questions, but they are exactly the ones that life insurance answers.

This guide is written to help you understand life insurance in plain, everyday language — no confusing jargon, no pressure selling. By the time you finish reading, you will know:

- What life insurance is and how it works

- The different types of life insurance plans available in India

- How to compare and choose the best plan for your specific needs

- Common mistakes that people make (and how to avoid them)

- How to get the most out of tax benefits linked to life insurance

Whether you are buying your first policy or reviewing an existing one, this guide will give you the clarity and confidence to make the right call.

What Is Life Insurance? A Clear, Simple Explanation

Life insurance is a legal agreement between you and an insurance company. You pay regular premiums, and in return, the insurer promises to pay a fixed amount of money — called the sum assured — to your nominated family member if you pass away during the policy period.

In some types of plans, you also receive a payout if you survive the policy term. But the primary purpose of life insurance is financial protection for the people who depend on you.

Why Does Life Insurance Matter in India?

According to data from the Insurance Regulatory and Development Authority of India (IRDAI), life insurance penetration in India stood at approximately 3.2% of GDP in 2023 — which is still quite low compared to developed countries.

This means a significant percentage of Indian families have no financial safety net in place.

The reality is that most Indian households rely on a single or dual income. Any disruption to that income — caused by death, disability, or critical illness — can push a family into serious financial difficulty almost immediately.

Life insurance exists to prevent exactly that situation.

Key Terms You Should Understand

| Term | Simple Meaning |

|---|---|

| Sum Assured | The amount paid to your family if you pass away |

| Premium | Your regular payment to keep the policy active |

| Policy Term | How long the insurance cover lasts |

| Nominee | The person who receives the insurance money |

| Maturity Benefit | The payout you receive if you survive the term (only in savings-based plans) |

| Claim Settlement Ratio (CSR) | Percentage of claims an insurer settled — higher is better |

| Free-Look Period | A window (15–30 days) to cancel and get a refund if unsatisfied |

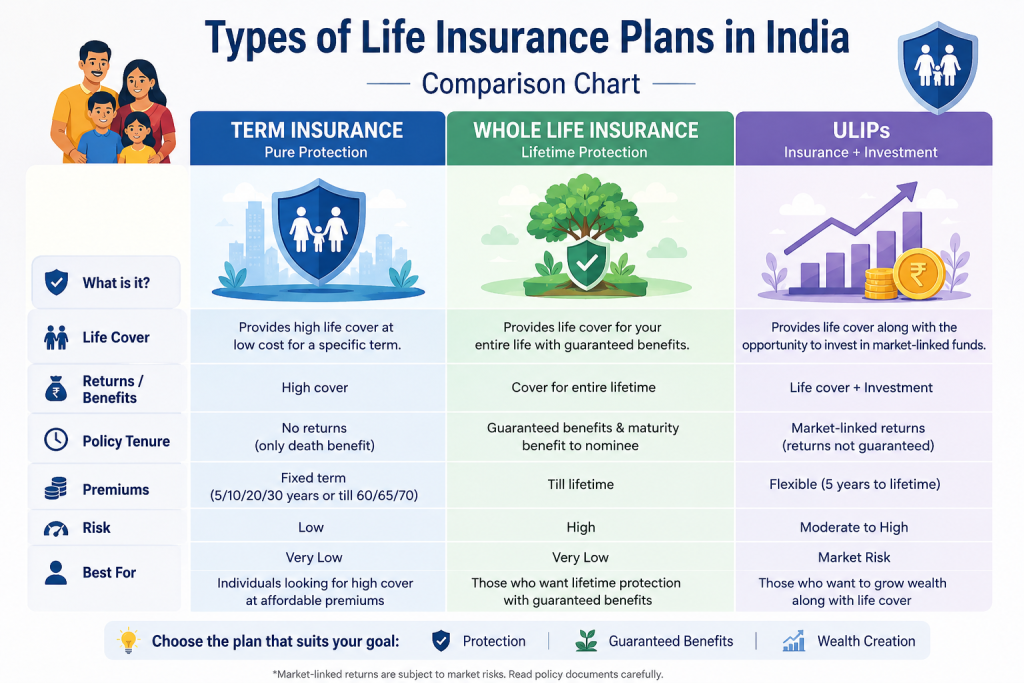

Types of Life Insurance Plans in India

Not every life insurance plan works the same way. There are several types, each built for a different purpose. Understanding these types is the foundation of making the right choice.

Here is a quick overview:

- Term Insurance — Pure life cover, no savings component

- Whole Life Insurance — Covers you for your entire lifetime

- Endowment Plans — Insurance + savings combined

- ULIPs — Insurance + market-linked investment

- Money-Back Plans — Periodic payouts during the policy term

- Child Plans — Secures a child’s financial future

- Pension/Annuity Plans — Provides income after retirement

We will focus in detail on the four most popular and widely used categories below.

Term Insurance — The Most Important Type You Need to Know 🔥

If there is only one type of life insurance you learn about today, make it term insurance.

Term insurance is the purest and most affordable form of life insurance available in India. You choose a policy term (say, 30 years), pay a relatively small premium every year, and your family receives the sum assured if you pass away during those 30 years.

There is no investment, no savings, and no maturity payout in a standard term plan. That is what keeps the premium low and the coverage high.

Why Term Insurance Should Be Your First Priority

A 30-year-old non-smoker in good health can get a ₹1 crore term insurance policy for as little as ₹700–₹900 per month. That is roughly the cost of a monthly subscription service — and it could be the most financially important thing you ever spend that money on.

No other financial product gives you this level of coverage at this price point.

Types of Term Insurance Plans

- Level Term Plan — Sum assured stays constant throughout the term

- Increasing Term Plan — Sum assured grows each year to match inflation

- Decreasing Term Plan — Sum assured reduces over time, ideal for loan coverage

- Return of Premium (ROP) Plan — All premiums returned if you survive the term (higher premium)

- Convertible Term Plan — Can be converted into an endowment or whole life plan

How Much Term Insurance Cover Do You Actually Need?

A widely used formula:

Ideal Life Cover = (Annual Income × 15) + All Outstanding Loans + Future Financial Goals

So if you earn ₹8 lakh per year, have a ₹30 lakh home loan, and want ₹20 lakh set aside for your child’s education, you should aim for a cover of approximately ₹1.7 crore or more.

Many people underestimate this number significantly.

What to Check Before Buying Term Insurance

- ✅ Claim Settlement Ratio — Look for 97% or above

- ✅ Solvency Ratio — Must be above 1.5 as per IRDAI norms

- ✅ Available Riders — Critical illness, disability, and premium waiver riders add value

- ✅ Exclusions — Read carefully what the policy does NOT cover

- ✅ Insurer’s Track Record — How long have they been in business? What do customers say?

Top Term Insurance Plans in India (2024–25)

| Plan Name | Claim Settlement Ratio | Standout Feature |

|---|---|---|

| Max Life Smart Secure Plus | 99.5% | Highest CSR in India |

| LIC Tech Term | 98.7% | Government-backed trust |

| HDFC Life Click 2 Protect Super | 98.4% | Flexible cover options |

| Tata AIA SRS Vitality Protect | 98.5% | Wellness rewards |

| ICICI Pru iProtect Smart | 97.9% | Comprehensive riders |

🔗 Compare term insurance plans: Policybazaar | Ditto Insurance

🔗 Internal Read: Beginner’s Guide to Financial Planning — Zyqorr.com

Whole Life Insurance — Coverage Without an Expiry Date

Whole life insurance does exactly what its name suggests — it covers you for your entire life, typically up to age 99 or 100.

Unlike term insurance, you do not have to worry about outliving your policy. Your family will receive the death benefit whenever you pass away, as long as the policy is active.

Additionally, whole life insurance builds a cash value over time, which you can borrow against or withdraw in certain situations.

Who Should Consider Whole Life Insurance?

- People who want to leave behind an inheritance or financial legacy

- Business owners who need permanent coverage for estate planning

- Families with lifelong dependents — such as a family member with a disability

Whole Life Insurance — Pros and Cons

| ✅ Advantages | ❌ Disadvantages |

|---|---|

| Lifelong coverage guaranteed | Significantly higher premiums |

| Builds cash value over time | Cash value growth is slow |

| Can be used as loan collateral | Complex policy structure |

| Certain death benefit payout | Long-term premium commitment |

For most salaried individuals in India, a term insurance plan combined with separate investments will be more cost-effective than whole life insurance. However, whole life plans serve specific needs very well.

Endowment Plans — Savings and Protection Together

An endowment plan is a life insurance policy that includes a savings component. At the end of the policy term, if you are alive, you receive a maturity benefit — your sum assured plus any accumulated bonuses.

If you pass away during the term, your nominee receives the death benefit.

How an Endowment Plan Works — A Simple Example

Ramesh, age 32, buys an endowment plan with a RS.10 lakh sum assured for 20 years. He pays rS.45,000 in annual premiums.

- If he passes away in year 8 → His family receives ₹10 lakh + bonuses

- If he survives 20 years → He receives ₹10 lakh + accumulated bonuses as maturity amount

Are Endowment Plans Worth It?

Endowment plans typically offer returns between 4% and 6% per annum — which is lower than mutual funds or even PPF. However, they offer:

- Guaranteed, safe returns

- Life insurance protection throughout

- Disciplined, forced savings

If you value security and discipline over higher returns, endowment plans can fit into your financial plan. But if wealth creation is your primary goal, they may not be the best standalone option.

💡 Pro Tip: Consider the “Buy Term and Invest the Difference” (BTID) strategy — buy a cheap term plan and invest the premium difference in mutual funds for potentially higher returns.

ULIPs — Market-Linked Insurance Explained

ULIPs (Unit Linked Insurance Plans) split your premium in two ways: one part goes toward life insurance coverage, and the other part is invested in market-linked funds such as equity, debt, or hybrid funds.

ULIPs combine the dual benefits of wealth creation and life protection in a single product.

How ULIPs Work

- You pay your premium

- Charges are deducted (mortality, fund management, admin charges)

- The remaining amount is invested in your chosen fund

- Fund value grows or falls depending on market performance

- After 5 years (mandatory lock-in), you can make partial withdrawals

ULIP Charges — Know Before You Invest

| Charge | Description |

|---|---|

| Premium Allocation Charge | Deducted from premium before investment |

| Fund Management Charge | Annual charge for managing the fund (capped at 1.35% by IRDAI) |

| Mortality Charge | Cost of the life insurance component |

| Policy Administration Charge | Monthly admin fee |

| Surrender Charge | Applicable if exiting within 5 years |

ULIPs vs Mutual Funds — Quick Comparison

| Feature | ULIPs | Mutual Funds |

|---|---|---|

| Life Cover | ✅ Yes | ❌ No |

| Lock-in Period | 5 years | 3 years (ELSS only) |

| Tax Benefit | 80C + 10(10D) | 80C (ELSS only) |

| Charges | Moderate-High | Low |

| Flexibility | Moderate | High |

| Best For | Long-term (15–20 yrs) | Any horizon |

🔗 Internal Read: Investment Basics for Beginners — Zyqorr.com

Best Life Insurance Plans in India (2025–26)

Here is a curated, category-wise breakdown of the best life insurance plans in India right now.

Best Term Insurance Plans

| Plan | CSR 2023–24 | Key Highlight |

|---|---|---|

| Max Life Smart Secure Plus | 99.5% | India’s highest CSR |

| LIC Tech Term | 98.7% | Most trusted brand |

| HDFC Life Click 2 Protect Super | 98.4% | Flexible options |

| Tata AIA SRS Vitality Protect | 98.5% | Health-based rewards |

| ICICI Pru iProtect Smart | 97.9% | Wide rider options |

Best Endowment Plans

| Plan | Insurer | Highlight |

|---|---|---|

| Jeevan Anand | LIC | Whole life cover post-maturity |

| HDFC Life Sanchay Plus | HDFC Life | Guaranteed fixed returns |

| SBI Life Smart Bachat | SBI Life | Flexible payment terms |

Best ULIPs

| Plan | Insurer | Fund Options |

|---|---|---|

| ICICI Pru Signature | ICICI Prudential | 11 funds |

| HDFC Life Click 2 Wealth | HDFC Life | 10 funds |

| Max Life Online Savings Plan | Max Life | 8 funds |

🔗 Compare All Plans: InsuranceDekho | Coverfox

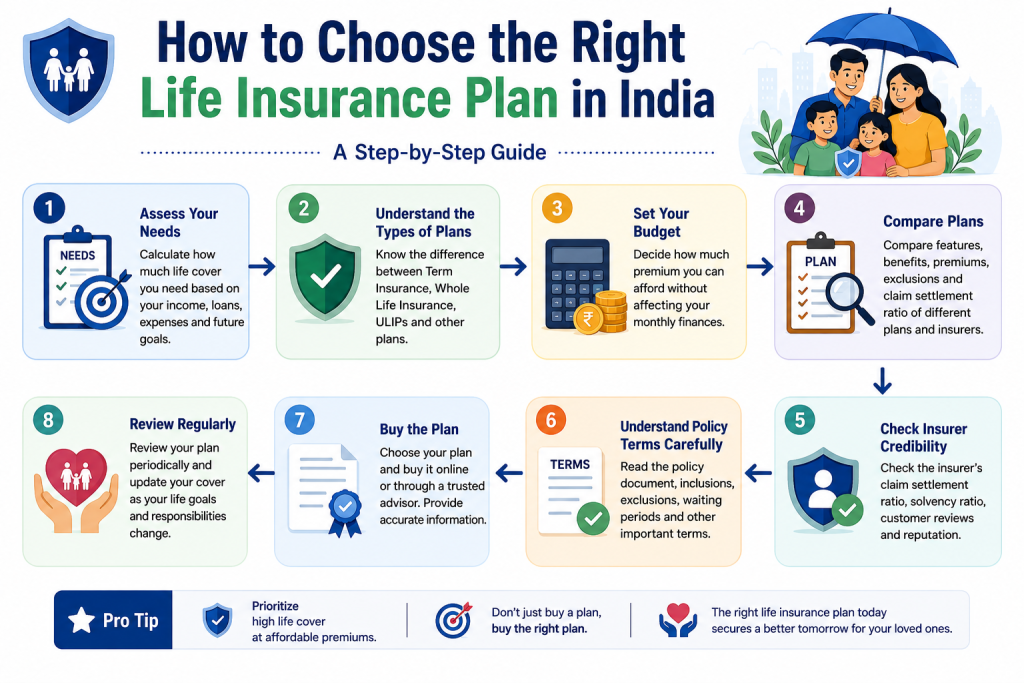

7 Proven Steps to Choose the Right Life Insurance Plan

This is the heart of this guide. Follow these 7 steps to make a confident, well-informed decision.

Step 1 — Define Your Goal Clearly

| Your Goal | Recommended Plan |

|---|---|

| Pure family protection | Term Insurance |

| Savings + protection | Endowment Plan |

| Wealth creation + protection | ULIP |

| Lifelong coverage | Whole Life Insurance |

Step 2 — Calculate the Right Cover Amount

Use this formula:

(Annual Income × 15) + Outstanding Loans + Future Goals = Ideal Cover

Do not go below this number.

Step 3 — Set a Realistic Premium Budget

Choose a premium you can pay without interruption for the entire policy term. A lapsed policy provides zero protection.

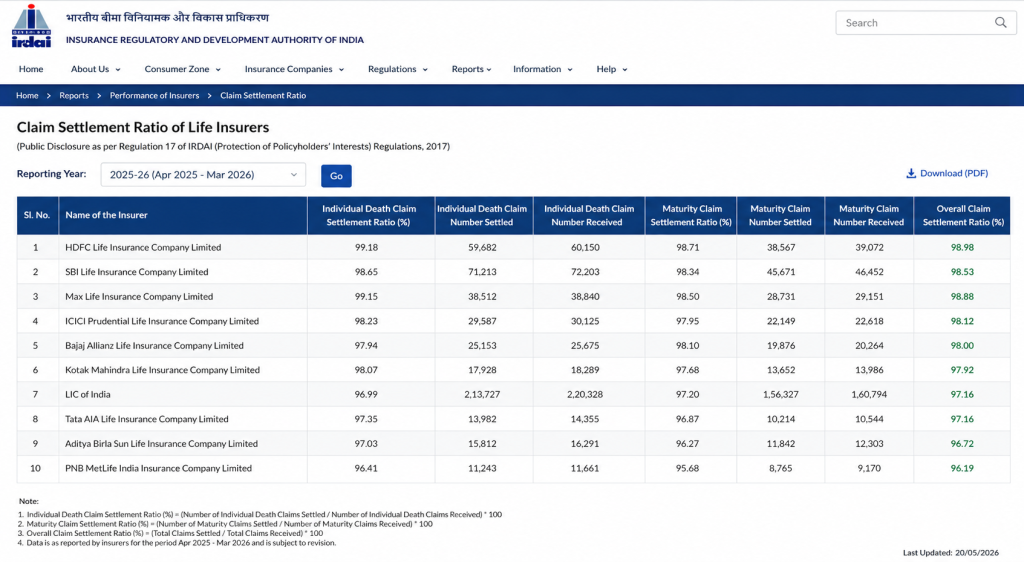

Step 4 — Verify the Insurer’s Claim Settlement Ratio

Always check the latest CSR data from the IRDAI Annual Report. A CSR above 97% is a good benchmark for reliability.

Step 5 — Add the Right Riders

Consider these valuable add-ons:

- 🛡️ Critical Illness Rider — Pays a lump sum on diagnosis of major illness

- 🦽 Accidental Disability Rider — Provides income if you become disabled

- 💸 Waiver of Premium Rider — Waives future premiums if you are disabled

- 💀 Accidental Death Benefit Rider — Extra payout for accidental death

Step 6 — Read the Policy Document Carefully

Pay special attention to:

- Exclusions — what situations are NOT covered

- Free-look period — your window to cancel without penalty

- Grace period — time allowed after missing a premium

- Revival terms — how to reinstate a lapsed policy

Step 7 — Inform Your Nominee Completely

Make sure your nominee:

- Knows the policy exists

- Has a copy of the policy document

- Understands how to file a claim

- Has the insurer’s helpline number saved

Benefits of Buying Life Insurance Early

Buying life insurance at a younger age comes with several real and measurable advantages.

- Lower Premiums: A 25-year-old pays significantly less than a 40-year-old for the same cover amount and term

- Easier Approval: Younger applicants typically have fewer health issues, making underwriting smoother

- Longer Coverage Period: You get more years of protection for your family

- Lock-In of Good Health: Any health issues that develop later do not affect your existing policy

- More Time for ULIP Growth: If you choose a ULIP, a longer investment horizon means compounding works harder for you

- Peace of Mind Earlier: You stop worrying about what would happen to your family, because you have already planned for it

Risks and Limitations You Should Know

Like any financial product, life insurance has its limitations. Being aware of them helps you plan better.

Limitations of Term Insurance

- No maturity payout if you survive (in standard plans)

- Cover expires at the end of the term — must be renewed or replaced

Limitations of Endowment Plans

- Returns (4–6%) are often lower than inflation-adjusted investment returns

- High premiums relative to the coverage provided

- Surrendering early results in significant financial loss

Limitations of ULIPs

- Market-linked — returns are not guaranteed

- Multiple charges can erode returns, especially in early years

- Requires a long holding period (15+ years) to generate meaningful returns

- Complex to understand and track

Limitations of Whole Life Insurance

- Highest premiums among all plan types

- Cash value growth is slow

- Returns on cash value are modest compared to direct investment

General Risks

- Policy lapse due to non-payment — you lose all coverage

- Non-disclosure of health information — can lead to claim rejection

- Inadequate cover — most people underinsure significantly

- Nominee not updated — causes complications at claim time

Common Mistakes to Avoid When Buying Life Insurance

These are the errors that cost people the most — financially and emotionally.

❌ Mistake 1 — Buying Too Little Cover

A ₹25 lakh policy for a person earning ₹12 lakh per year is dangerously insufficient. Always calculate your actual coverage need — not what feels affordable.

❌ Mistake 2 — Waiting Too Long to Buy

Every year you delay means higher premiums and more years without protection. There is no perfect time — the right time is always now.

❌ Mistake 3 — Hiding Health Information

This is the single biggest reason for claim rejections. Insurers investigate at the time of claim, not at the time of purchase. Always disclose all health conditions, smoking habits, and family medical history honestly.

❌ Mistake 4 — Treating Insurance as Investment

Insurance and investment serve different purposes. Mixing them (through endowment plans or ULIPs) can work, but only if you understand the trade-offs. Do not buy an endowment plan expecting mutual-fund-level returns.

❌ Mistake 5 — Ignoring Riders

Riders like critical illness cover or waiver of premium cost very little extra but can make a massive difference in difficult situations. Do not skip them to save a few hundred rupees.

❌ Mistake 6 — Never Reviewing the Policy

Life changes. Your income grows, you take on new loans, you have children. Review your life insurance coverage every 2–3 years and top it up as needed.

❌ Mistake 7 — Choosing Based on Premium Alone

A policy with a lower premium from an insurer with a poor CSR can be far more dangerous than a slightly costlier policy from a more reliable insurer. Always weigh multiple factors.

Expert Tips Before You Buy

These are insights gathered from certified financial planners and insurance advisors across India.

Tip 1: “Always prioritize a pure term plan before buying any other financial product. Once your family is protected, then think about investments.” — Common advice from SEBI-registered financial advisors

Tip 2: Buy term insurance online directly from the insurer’s website or a trusted aggregator. Online policies are typically 10–15% cheaper than offline policies.

Tip 3: Do not combine too many riders — choose only those that genuinely fill a gap in your financial protection.

Tip 4: Check whether your insurer has a mobile app and a smooth digital claim process. In stressful times, ease of claim filing matters enormously.

Tip 5: If you are self-employed or a business owner, consider a higher cover amount since you do not have employer-provided group insurance as a backup.

🔗 Internal Read: Risk Management for Beginners — Zyqorr.com

Tax Benefits of Life Insurance in India

One of the practical advantages of holding a life insurance policy in India is the meaningful tax relief it provides.

Section 80C — Deduction on Premiums Paid

Premiums paid toward life insurance policies qualify for a deduction of up to ₹1.5 lakh per year under Section 80C of the Income Tax Act, 1961.

This applies to:

- Term insurance premiums

- Endowment plan premiums

- ULIP premiums

- Whole life insurance premiums

Section 10(10D) — Tax-Free Maturity and Death Benefits

Proceeds received from a life insurance policy — whether as a death claim or maturity payout — are completely tax-exempt under Section 10(10D), subject to conditions:

- Premium must not exceed 10% of sum assured (for policies issued after April 1, 2012)

- For ULIPs: annual premium must be below ₹2.5 lakh for tax-free maturity

GST on Life Insurance Premiums

| Plan Type | GST Applicable |

|---|---|

| Term Insurance | 18% on premium |

| Endowment Plan | 4.5% (Year 1), 2.25% (subsequent years) |

| ULIPs | 18% on charges |

⚠️ Note: Tax laws are subject to change. Always consult a certified chartered accountant or financial advisor for personalized advice.

FAQs About Life Insurance

Q1. What is the ideal age to buy life insurance in India?

The ideal age is as early as possible — ideally between 25 and 35 years. Premiums are lower when you are young and healthy, and you lock in those rates for the entire policy term. Most insurers allow buyers from age 18 onwards.

Q2. How much life insurance cover is enough for an average Indian family?

A general rule is 10 to 15 times your annual income, plus any outstanding loans and future financial obligations like education or marriage costs. For a person earning ₹10 lakh per year with a ₹40 lakh home loan, a cover of at least ₹1.5–₹2 crore is advisable.

Q3. Can I have multiple life insurance policies?

Yes, you can hold multiple life insurance policies from different companies. Each policy will pay independently at the time of a claim. However, you must disclose all existing policies when applying for a new one.

Q4. What is the claim settlement ratio, and why does it matter?

The Claim Settlement Ratio (CSR) is the percentage of death claims that an insurer actually paid out during a given year. A higher CSR means the insurer is more likely to honor your family’s claim without disputes. Look for insurers with a CSR of 97% or above.

Q5. What happens if I stop paying my life insurance premium?

If you miss a premium, most insurers offer a grace period of 15–30 days to pay without the policy lapsing. If you miss that too, the policy lapses and coverage stops. Most policies allow revival within 2–5 years by paying overdue premiums with interest. Do not let your policy lapse.

Q6. Is term insurance worth buying if I never make a claim?

Absolutely. Term insurance is like a seatbelt — you hope you never need it, but it is essential. If you value your family’s financial security, the premium you pay is the cost of that peace of mind. You can also opt for the Return of Premium (ROP) variant if you want to receive your premiums back at maturity.

Conclusion

Life insurance is not a product to be delayed, ignored, or minimized. It is the foundation of a sound financial plan for anyone who has people depending on them.

Here is what we covered in this guide:

- Term insurance is the simplest, most affordable, and most impactful type of life insurance — it should be your first priority

- Whole life insurance works best for estate planning and lifelong financial obligations

- Endowment plans offer a blend of savings and protection, with lower but guaranteed returns

- ULIPs combine market-linked investment with life cover, best suited for long-term goals

- When choosing the best life insurance plan in India, check the CSR, read the exclusions, pick the right cover amount, and never underinsure

- Tax benefits under Section 80C and 10(10D) make life insurance even more financially attractive

- Start early, stay consistent, review regularly, and keep your nominee fully informed

The right life insurance plan is not the cheapest one or the most feature-packed one — it is the one that genuinely fits your family’s needs and ensures they are protected no matter what life brings.

Also Read: Insurance Basics: 7 Essential Things Every Smart Person Must Know

⚠️ Financial Disclaimer

This content is for educational purposes only and should not be considered financial advice. Life insurance products, premiums, claim settlement ratios, and tax rules mentioned in this article are subject to change. Always conduct your own research and consult a certified financial advisor or insurance professional before making any financial decisions. Zyqorr.com does not sell insurance products and is not affiliated with any insurance company mentioned in this article.

{kind=link}